2 Branch Expansion Lessons from the Bank of Frankewing

- Branch Transformation

Categories:

In branching, especially in this day and age, there is no definitive answer for the right formula of a bank or credit union. Every single branch should be unique according to each financial institution. This includes the idea of branch expansion.

There is much to be learned by understanding what others are doing, however. Adopt those lessons to fit your strategy when they apply.

Enter the Bank of Frankewing. It is located in the town of Frankewing, Tennessee, near the Alabama border. The bank was interested in expanding its footprint into Alabama to take advantage of the explosive growth on the north side of Huntsville.

The bank contacted LEVEL5. In addition to a full corporate headquarters remodel, they decided to build a new branch in Hazel Green, Alabama. There, what used to be cotton fields gave way to explosive growth from those moving out of Huntsville who were still close enough for their daily commutes back into town.

Of the many decisions that led to that branch, there are two critical strategies that the Bank of Frankewing undertook. They are valuable lessons for those looking to expand their branch footprint.

LESSON #1 – Open a “Branch” Before Opening the Branch

As you’ll see in the photos, the Bank of Frankewing made a very smart decision. They placed a mobile trailer (you can even call it a Micro Branch) on the site of the new branch. The mobile branch has all of the critical features. It has a 3 full-time staff, a drive-thru, ATM, but most importantly, the ability to not only serve current customers in this market, but to also open new accounts and increase loans and deposits.

Through a very targeted and strategic marketing plan, the Bank of Frankewing marketing team executed a campaign to let those current customers know that not only was there going to be a very impressive branch operating in their community, but that the trailer was acting as a branch unto itself for any financial needs. Furthermore, the marketing campaign also spoke to non-customers. It was important to let them know there was a new financial player in the market.

Though the permanent branch is still several months away from completion, the bank has already exceeded its loans and deposits forecasted from the mobile “Micro Branch.”

LESSON #2 – Turn Your Branch Into a Regional Hub

In an age where branches have become smaller due to technology, the Bank of Frankewing did not worry about trends. Rather, they made decisions that were right for them. The new branch represents two stories, and nearly 12,000 square feet of space. The first floor will represent a traditional branch. The second floor will offer office space not only for product and service expansion, but for a Regional Hub within. You see, this branch in this town is not only a fair distance from the corporate office, but represents an anchor for future growth into Alabama. It will therefore act as a regional anchor for operations in the larger geography.

In branching, there is not one size fits all approach – strategic decisions must be right for your institution.

If you’re interested in learning more about the Bank of Frankewing, and how LEVEL5 can help you craft and execute branch expansion strategies, Contact Us today to get started.

Keeping Your Facilities Lean and Green

- Branch Transformation

Categories:

As the world begins to thaw from our very long winter, a bright and warm Spring is on the horizon.

The grasses and trees have begun sprouting their respective shades of green.

Now, employees are beginning to return to their workplaces from a long, COVID-inspired hibernation. Here, we highlight 6 “green” trends that you can implement in your workplace to not only welcome your employees back, but freshen it up and make it more environmentally conscious.

Energy Efficient Lighting

Compact Fluorescent Lighting (CFL) or Light-Emitting Diode (LED) bulbs are no longer a novelty – they may very well be expected. If your employees have been away for a while, it’s as easy as changing a light bulb.

ENERGY STAR HVAC

ENERGY STAR certifications for your HVAC systems offer a more efficient, and thus, more “green” solution.

And it’s not just about the environment – you can see up to 30% in savings on your heating and cooling costs.

Environmentally Conscious Design

From window placements, skylights, solar panels, geothermal systems, and even recycled building materials, there are many ways to add Design elements both inside and out for a better building. We have designed and built many buildings where energy efficiencies become front and center. Our solar and heat mapping software can predict temperature fluctuations during time of day, and time of year – giving you visibility into what design choices need to be made to cut down on cooling costs.

Water Conservation

Water waste is a real thing. There are very simple measures that can be taken to lessen the overall water waste, and even ways to capture rainfall for your building’s use.

On the interior, make smart choices such as low-flow toilets and motion-sensor faucets that turn on/off automatically and do not run the risk of being turned on and left on.

For exterior landscaping, work with your Design firm to seek out trees, plants and shrubs that require less water. Drought tolerant plants are a big bonus here such as Cactus and Succulents.

Finally, you could consider adding industrial-sized Rain Barrels. These can look pretty cool, but they also have tremendous benefits in storing its water for use around the property.

Eco-Friendly Materials

With the properly rated insulation panels, operational costs can be positively impacted by keeping the building cooler in the hot months, and warmer in the colder months.

Additionally, reflective paint can, well, reflect the baking sun, limiting the warming effect on exterior walls.

Green Roof

The final “green” idea is to add more green to your building.

While it may sound crazy, take inspiration from our Hobbit friends in Middle Earth and actually have grass on your rooftop. This “living roof” has many benefits, from an overall cooling effect to increasing a roof’s lifespan by up to 200%.

Additional rooftop ideas would be to add a planters or even a garden. Depending on the building and rooftop/terrace access, this “community garden” has a big upside on the environment. It may be a very cool crowdsourcing idea for your employees to build, tend, and benefit from what is grown.

If you’d like to learn more about ways to go Green, Contact Us today.

We’re Already Right

- Banks

- Branch Transformation

- Credit Union

- Retail

Categories:

Well, that didn’t take long.

We’re not one to gloat, but we do know what we’re talking about.

In looking at some industry publications and comparing it to our Crystal Ball series posted over the past two weeks, there are two very interesting tidbits that have hit the wires that back up and corroborate our thoughts on the year to come.

Point #1 – The Branch Matters

Throughout the past year, there has been news of PNC, Chase, and others closing branches. Despite this and the tailspin that all of retail was caught in due to the pandemic, it has been proven that the branch still matters.

In fact, according to a recently conducted Novantas survey published by American Banker, “Despite the increased adoption of digital banking, branches still matter to consumers as they select which institution they want to bank with, research has shown.”

Furthermore, a recent Forbes Article states that while the pandemic has impacted branches, they still remain important, only possibly, and likely evolving (which they were regardless).

Despite headwinds, the branch is still a critical component. Clients want to meet in person for transactions such as account openings and decisions on which institution to bank with. It is a critical component to a well-planned and executed omni-channel strategy.

So, don’t take our word for it – other independent periodicals are saying the same thing.

While digital and FinTech get all the headlines, the branch is still the anchor point for consumer FI’s.

Point #2 – Digital Only Is Not That Simple

Speaking of digital – yes, you click on the articles and yes, you are intrigued. You should not become a “digital only” brand, though.

In recent news, BBVA announced that it is Shutting Down Simple. The online-only banking app is to begin migrating all users into the standard BBVA digital ecosystem.

So, what to make of this? Digital is important, but it’s not the single answer. Similar to the point made above (and in our Crystal Ball series) a well balanced omni-channel strategy is the right approach. Investment weights in the channels can ebb and flow year over year, but, over time, they should even themselves out.

If your digital experience is lacking, it’s time to get it up to par. You will not outcompete the big banks, nor should you pivot and try to become the next FinTech darling. Simple already wore that crown and look at where it is now – a footnote.

Would you like to speak with an expert regarding your branch strategy and how to balance your customer channels? The experts at LEVEL5 are ready to speak with you today.

A great place to start is with our data driven Consulting Group, who can assess your branch network and help you make the right decisions – Contact Us today to get the conversation going.

2021 Crystal Ball: Boldly Predicting the Year to Come – Full Article

- Branch Transformation

Categories:

It’s that time of year again. This is when we look ahead to stick our necks out and make bold claims predicting the year to come.

While we don’t claim to be soothsaying, we do have the crystal ball and know how to interpret its readings. So here, in a two-part series, we outline trends and share our thoughts on what is to come. This way, you can interpret and translate accordingly for your 2021 strategic plans.

Branch Matters

While saying the branch will change is an obvious statement on the surface, as any retail setting inevitably ebbs and flows with the times, these are most unusual times. It’s no mystery that the COVID-19 has altered the course of banking, retail, and the economy as a whole.

What began to unfold in mid to late March 2020 was reactionary. It was a triage of our retail facilities (and employee facilities) as impact was still unfolding. While the impact of the pandemic is still very much at play in our daily lives, enough time has transpired to understand its effect on our businesses. 2021 retail strategies need to incorporate COVID’s legacy.

Aside from the simple and expected sanitization stations, the branch needs to evolve for a post-pandemic world. If an “open concept” branch was just a trend

previously, it is a necessity now. While there may come a day when social distancing is not mandated, it will remain a practice with a long hangover in our collective consciousness. Your branch layout needs to accommodate for it.

While some believe that traditional Teller Lines still have a place in the branch, Teller Towers are at the forefront like never before. These pods, with the right Banking Equipment, enable a more open floor plan while eliminating the old-school queuing.

Rise of the Machines

No, we’re not talking about robots inheriting the earth. The right blend of technology will modernize your branch, enhance the overall retail experience, enable social distancing naturally, and make traditional in-branch transactions that much more efficient.

The right blend of technology, both in and outside of your branch, will enhance the overall customer experience. This, in turn, will further justify the need for branch visits.

Teller Cash Recyclers work perfectly affixed to a Teller Tower. It enables Universal Tellers to man these stations while also giving them the flexibility to walk about the branch.

Interactive Teller Machines have been a much discussed and much contemplated piece of technology. Now, they have as much justification as ever before with the Renaissance seen in the drive through. ITMs in your drive-through give visitors the transactional need while also allowing for an interactive experience, albeit virtually.

The Omni-Channel Dilemma

It is no secret that digital transactions have risen since the pandemic hit last Spring. The reliance on digital methods became the only option when branches closed. Those who were reluctant to take advantage of simple transactions and information via Online Banking portals or Apps were forced to do so out of necessity and lack of options.

What is more surprising, though, is that in-branch transactions, particularly those involving account openings, has nearly, if not entirely rebounded to pre-pandemic levels.

So the question is: Do you invest in the Branch, or do you invest in your Digital Channels?

When you come to a fork in the road… take it. By this we mean, you should be investing equally in your offline and online channels. You always should have been.

Digital products and technological marvels get all the headlines. A more balanced omni-channel approach to your clients, however, has always been the right answer.

Sure, budgets may swing in favor of digital one year, then back to the retail branch the next. This is all a balancing act in what should be an equally weighted customer touchpoint strategy that unfolds over the course of many years as part of a well-executed three, five, even ten year strategic plan.

Executing this accurately, thoughtfully, and strategically, gives you a well-executed customer experience.

Experience Good Experience

If you have any web or app developers on your team, or if you’ve ever in a development meeting, you’ve heard words like “frictionless” and “UX.”Gone are the days of bloated and cavernous digital engagements. A digital design wants as few dead ends and wrong paths as possible, providing a frictionless experience. UX, or User Experience, is king when it comes to designing a new website and smartphone application. Extensive planning happens before any code is written or deployed.

Your branch should be no different. If the idea of a good customer experience in your retail setting is news to you, it is not too late. The branch is going through an evolution the wake of the pandemic. Now, more than ever, you truly need to be thinking engagement and experience first when it comes to your branch.

The branch is important, and while digital channels should not be seen as a replacement for functions in the branch, they should be complimentary and designed equally from a UX perspective.

Give your visitors a reason to continue to come in. Whether it be traditional transactions or advisory sessions, the branch is still an important piece in your omni-channel strategy.

Allow the right technology to perform transactions. The right staff on point to answer the right questions, and, more importantly, open accounts, is where your branch should really shine.

Blending transactions and advisory services into a seamless retail experience is the right approach.

If you would like to jump into addressing some of your glaring branch shortcomings, our Re-FI Design Program is the perfect anecdote to an outdated branch.

The Great Migration (Back to Work)

Just as giant herds of wildebeest seek greener pastures, your employees too will return from whence they came.

While the pandemic continues to steal headlines and as I continue to write this article, cases are as high as ever. Branches hours are changing daily, but there is light at the end of the tunnel. Whether it’s due to warmer temperatures, vaccination roll outs, or herd immunity, many believe the pandemic’s peak is upon us. The downward curve is fast approaching and health and business experts alike agree that the post-pandemic world is within reach.

Your employees, who are still working in their home offices, kitchen tables, or closets under the stairs, will have to physically return to their places of employment. It could be on a flex schedule or full-time basis. No matter what, though, they are returning and you and your organization must be prepared for them.

Aside from some bottles of sanitizer, chances are that your corporate offices are not prepared for a proper return. Do your current offices need to be renovated accordingly? Are you looking into the future for an entirely different office building? If so, we have created the “L5 HQ” program, which is meant to assess your corporate office needs.

The Cost of Things

The cost of doing business, specifically in the Design-Build world, has been greatly impacted by the pandemic. As we look ahead to 2021, there will be carryover from 2020 along the following fronts:

Labor

One of the ironic impacts from the pandemic has been the boom to the construction industry. If you have not done something to your home, the chances are, your neighbor has. Ever since the first wave of lockdowns commenced back in March, there was a massive rise in DIY projects. All of a sudden, desires arose to landscape yards, update kitchens, overhaul master baths, finish unfinished basements (guilty), and build out those home offices.

While on the surface, this all sounds residential and not commercial, an impact on labor is seen across sectors. You see, the crew doing your home project may also be the sub-contractor at the complex up the road.

Thus, we have a national labor shortage, with states like New York, Florida, California and Texas particularly feeling the pinch.

This is where planning ahead and having the right General Contractor for your branch or headquarters project really count.

The right GC has existing relationships with the local sub-contractors who pour the concrete, set the framing, and manage all the other elements that make up your building. Subs tend to allow themselves to be hired out by those they trust, and those who feed them continued work. A local General Contractor typically does not have the pull and project load compared to a national outfit.

Materials

So, if there is a labor shortage, that must mean that there are many projects abound and materials are in short supply. When supply is short, costs go up. Timber in particular has struggled to keep up with demand. While our projects continue to stay on budget, we are aware of the national timber shortage and have seen it impacting jobs across the country.

Regardless, post-pandemic prices have not dipped, but are instead rising slightly. There will likely be a leveling off by mid-summer. Projects in the construction industry have stayed steady, however.

Q&A RE M&A

I sat down with our lead consultant, John Hyche. His reputation as a thought leader in the industry has continued throughout his nearly 30-year career. John is no stranger to Mergers and Acquisitions, having been involved in heading many consulting engagements with clients over the years.

I asked John his thoughts regarding Mergers and Acquisitions and the below is a summary of his thoughts:

Mergers and Acquisitions will continue to be a trend within the industry. While the pandemic and post-pandemic world has its influence, the trends and reasonings behind the topic are consistent.

They can be broken down into 3 broad categories.

The first we’ll call “The Smaller Players.” These community based FI’s are typically operating a small handful of branches in their comfortable corner of a given market, with assets in the single digit millions to low double digits. They are surrounded by larger players, both in asset size, branch network and most importantly, efficiencies. The smaller players may ultimately find themselves at a precipice, where the cannot grow. Conversely, they may fill a niche for a local larger player, and so a M&A play commences.

The second scenario we’ll call “Merger of Equals.” This is when two like FI’s see complimentary components with one another. They may be similar, but also are seen as filling in gaps to one another. Whether it be geography (east side of town vs. west side), innovations, product offerings, customer base, etc. A merger of these “equals” is seen as a much faster growth route than doing it organically. This makes a lot of sense, but a critical component to the post-merger success is the personnel, with many organizations struggling to right-size their staff after the fact.

The third broad scenario we’ll call “The De Novo.” This is a new FI, from scratch. The advantage that a De Novo bank or credit union has is they can build whatever type of FI they want. They are not burdened by being branch first, tech first, on an old core system, or operating in the wrong trade areas. While De Novo FI’s may begin existence by filling a void in the market, ultimately, they may cause enough of a fuss for the bigger players in the market to begin to entertain an acquisition play. In fact, this may very well be the de novo strategy all along.

So there you have it, our Crystal Ball for 2021.

If you’d like to learn more, need to discuss your corporate office, or interested in our M&A Consulting Packages, Contact Us today.

Demystifying Pre-Construction

- Branch Transformation

Categories:

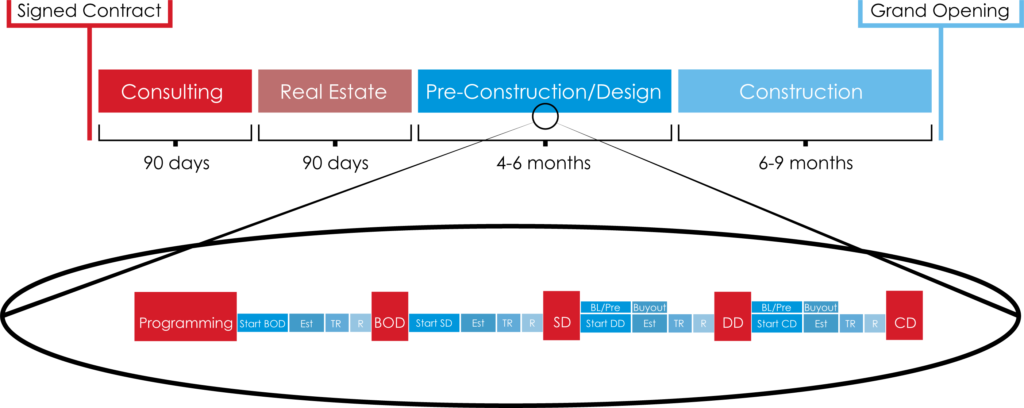

When you’re a Design-Builder, there are frequent discussions about the design and construction phases of a project. Many do not realize, however, that any good project begins with a “Pre-Construction” phase. This is composed of a series of purposeful steps geared toward complete alignment before any hammer swings.

Here, we give an introduction to the key steps in the LEVEL5 Pre-Construction phase:

Programming – Once the scope of a given project comes to light, and perhaps the market analysis is complete, the Programming phase of a project can officially commence.

At this point, LEVEL5 has probably conducted a deep-dive questionnaire with your organization. The questionnaires and series of interviews uncovered during the Consulting phase help set the right path with informed data for the right decision. We revisit the questions in the Programming phase, though. A whole new host of questions and deep-dives join them in an effort to lay the foundation of what will eventually become your project.

The reason the Programming is so thorough and important is that it is all about building your budget.

We discuss every zone in the branch or office building, make design choices, and discuss furnishings and finishes.

With this outlined in the Programming document, your team will review for accuracy and receive a budget aligned to scope.

Once this is entirely done and signed off, the next phase begins.

Basis of Design (BOD) – The Basis of Design is exactly what it sounds like, a baseline, or foundation for the final design to come. The renderings and floor plans delivered in this phase are the embodiment of everything captured in the Programming phase. They are early stage drawings, however, and likely will be different than the final drawings.

In addition to the early drawings, we will continue to carry the budget and anticipated project schedule through for visibility.

Schematic Design (SD) – This stage represents the first true evolved design. It will demonstrate the initial feedback from the drawings put forth at the Basis of Design. This stage includes the Architectural Site Plan, Floor Plan and Exterior Elevations.

Design Development (DD) – The renderings continue to evolve here. Now, they represent the critical juncture when drawings go from a conceptual evolution to sitting on the cusp of being finalized as Construction Drawings. This stage includes Engineering Documents, Wall Sections, Furniture, Exterior and Interior Renderings.

Construction Drawings (CD) – The final stage of the Pre-Construction phase is the Construction Drawings.

We package all aspects of the build for permitting and local jurisdiction requirements.

The project build begins once you and external entities approve these set of drawings.

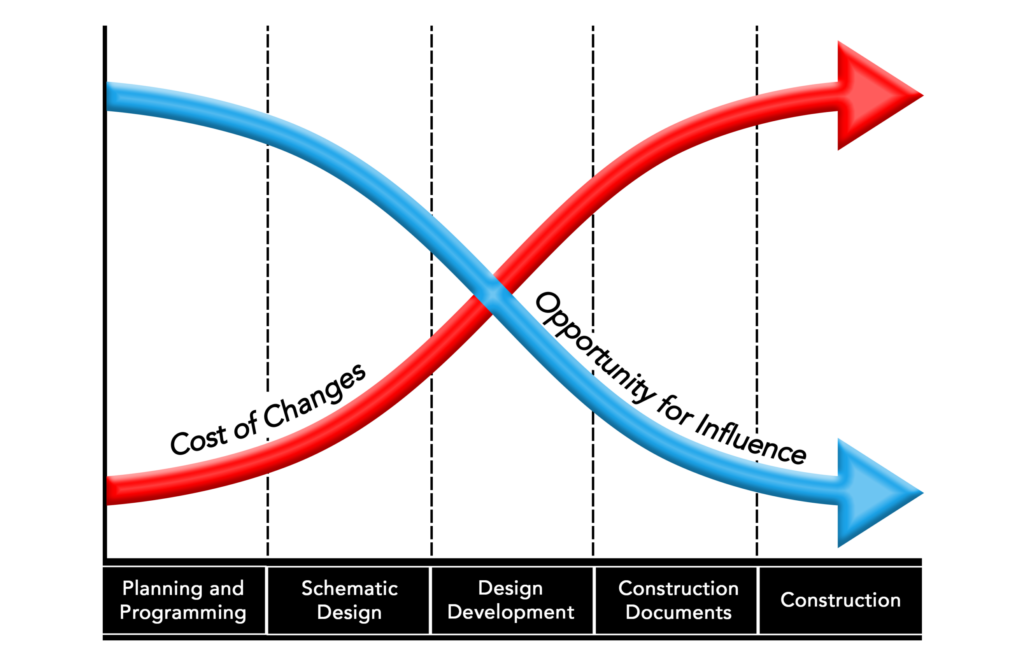

The reason Pre-Construction is important for you to understand not only to understand the flow and terminology, but more importantly, to understand your impact and influence on budget.

Although we will give you a budget after the Programming phase, that number can change for numerous reasons.

BUT, as the Pre-Construction phase continues, each successive phase represents a decreasing ability to maintain and impact the overall budget. As seen in this graphic, the influence of change decreases while your cost of change goes up throughout the timeline.

If you’d like to learn more about the Pre-Construction process, and any of our projects that have used this so effectively to maintain budget integrity, Contact Us today.

Feast Your Eyes On This “Crazy” Concept

- Branch Transformation

Categories:

Forgive me if you’ve heard us say this before, but when looking at branch design trends you should NOT look to the big boys. Particularly in the wake of the pandemic, you should not be focusing on Capital One with their cafes, Chase, BofA, Wells, or Citi with their grandiose, tech enabled, robot welcoming branches in the heart of the city.

We’ve been saying for a while now that trends in banking, particularly at the Community Bank and Credit Union level, should be looking at what “Quick Serve Restaurants” are doing with their drive-thru’s, curbside pick-up, and in-store transactional models.

On top of what we’ve discussed related to Target (http://level5.com/target-again-outlines-the-future-of-retail/) and our own designs regarding Curbside Banking (http://level5.com/curbside-banking-a-design-guide-supplement/) we now present you design concepts for “El Pollo Loco.”

This California based chicken restaurant has just unveiled their new store concepts. It is a direct result of a post-COVID world, where fast, convenient, and now “contactless” are paramount.

The highlights of the video are to demonstrate the adoption of key features, which are completely translatable to a branch:

Walk Up – Of course this makes sense for a place selling food in a bag, but the idea of a “walk up” is not new to banking, particularly in a Micro Branch concept. This has been used successfully in mobile Micro Branches, used in tight urban areas and at festivals. There’s no reason to believe that a walk up window cannot be deployed even at a flagship branch.

Drive Thru – The drive thru is nothing new. Pre-COVID, there were questions surrounding the long term viability of the idea, more specifically with the tubes. Now, the drive thru is having a new dawn, with many people still going to the branch, but opting for the drive thru’s ITM’s.

Open (Air) Concept – Open concept is not new. The advent of the cash recycler eliminated the need for the traditional teller line, which introduced the pod, which introduced the open concept floor plan. Now, branches have gone a step more by introducing retractable walls and rollups, bringing in fresh air, and peace of mind.

Curbside – The aforementioned curbside banking concept. Tech enabled, park in a spot, talk, seek advice, conduct transaction. Even have a Teller come out, if need be.

If you are curious about re-envisioning your branch for a post-COVID world, we have developed the Re-FI Program as a no obligation way for us to review your branch strategy and provide you with a budget and actionable items to set yourself up for a strong 2021 and future beyond.

3 Easy Steps

Simply Let Us Know You’re Interested

Our Team Will Call You To Discuss Needs

Our Design Team Will Review Existing Plan, Discuss Project Scope

Get Started Here

Beware The Frankenbranch

- Branch Transformation

- Retail

Categories:

We’ve all got ’em. That “branch on the hill” that just doesn’t quite fit into your overall branch network. It’s not well placed, likely in the wrong trade area, well past its prime, and looks nothing like any of your other branches.

It’s your Frankenbranch.

The design is stale, likely from a bygone era where the choices seemed fine at the time. It’s as dated as that can of Tab Clear nesting on your garage shelf next to your neatly stored sky blue tuxedo shirt with extra ruffles, cuz, just in case.

The single ATM is the lone piece of “tech.” The Brand Deployment may be a previous version of the logo design, if not definitely fading in color and importance.

In reality, this branch is not truthfully as scary as it is embarrassing.

Take solace in this: everyone’s got one.

You, as a manager and leader of a Financial Institution, make a point of assessing your organization’s talent pool, identifying the high potentials and underperforming. Why don’t you do the same for your branch?

If it’s about the economics and performance, the right analysis can aid in the tough decisions to relocate or shut down this monster.

How about if it’s an underperforming branch in the right Trade Area surrounded by high value clients? This is where a little love can turn this Frankenbranch into branch that is “ready for its close up.”

But don’t fret, there is good news.

If you want to analyze the market – LEVEL5 does that.

If you want to remodel your branch, maybe even turn it into your new flagship, if not your new prototype, well, we do that too.

Contact us today and we’ll help you give that monster of a branch a makeover that’ll make you, your board, and especially your clients happy.

Target (Again) Outlines the Future of Retail

- Branch Transformation

Categories:

.Here at LEVEL5, we know how to design and build branches, but you knew that already.

What you may not know is, while we’re experts at retail banking, we also stay up-to-date with design in general. We look at trends and take inspiration from hotels, bars, restaurants, clothing stores, and yes, big box retailers like Target.

In a recently published article from Fast Company (https://www.fastcompany.com/90103087/how-target-is-redesigning-to-take-on-amazon), Target has begun to outline what their next wave of store design will look like, but more specifically, how the design is giving way to the overall customer experience.

While the root of Target’s strategies are a direct reaction to the influence of Amazon and digital shoppers, here, we’re going to look at the three main design strategies from the retail banking lens and how these concepts could be interpreted in a new branch design.

A TALE OF TWO STORES

What Target Is Doing

Having two main entries is nothing new for Target, or even the likes of Walmart. When you have stores in excess of 100,000 square feet, two main entries is a no-brainer. The new store designs, however, will utilize the two different entry points into what strategically translates into two different stores under one roof.

If you frequent a Target nowadays, you likely know the overall store layout and which door to enter. Groceries, pharmacy, electronics, clothing, etc, all have a place in the overall planogram and you enter a given door based on ease of access to that department.

Now, Target is splitting up the store by intent. Do you want to browse or do you want to grab-n-go?

The difference here is between wether you want to spend some time and discover or whether you know exactly what you need to do. If you want the latter, you want it as quickly and efficiently as possible.

Translating This Into Retail Branching Terms

So, how does this now bifurcation in the customer shopping experience translate to the branch?

In today’s typical retail model, the branch has single door entry (on occasion two). The “transact zone” is the strategic anchor of a branch design and often at the center of the branch. Whether it be a traditional teller line or the more modern Teller Pods with Cash Recyclers, this “cash in, cash out” mechanism is seen as the primary reason for foot traffic. It is positioned as the first thing a customer sees upon entry.

Look at the new Target design and how it can translate to the branch. Layer on the how COVID-19 influenced change in the branch. It is not too difficult to see how a line in the sand can be drawn between delivering on a customer experience rooted in two notions of intent.

Grab-N-Go = Transact

With two strategically oriented hemispheres in the branch, the cash transaction would move to one side of the branch. It would no longer be the center focal point. It can still be positioned well enough for ease and good line of sight upon entry. By moving it to one side of the branch, however, it eliminates any cross pollination of those visiting the branch for non-transactional services.

Browse = Advise

Even before COVID-19 hit, the branch was undergoing a transformation. Digital transactions were on the rise. While the need for the neighborhood branch was still strong, these centers were proving to be more advisory and anchors for account creation instead of cash transactional.

To this end, the other side of this assumptive branch design would see a more advisory and “browse oriented” strategy. Customers can enter the branch, speak to a Universal Teller, discuss their financial needs, discover products and services though technology, and not worry about the short-lived nature of a transactional visit.

A MODERN DESIGN

What Target Is Doing

As described in the article, the new Target stores will take a more modern approach than before. They will migrate away from the old-school “warehouse” style that Walmart still deploys.

Expect to see more natural design elements, with woods, neutral and natural tones. You might even see stone in addition to some of the classic elements still needed in a big box store.

Translating This Into Retail Branching Terms

While a more modern design is nothing new for branches, this design move further solidifies the overall design aesthetic evolution happening in retail, but for banks, it also further solidifies the old, dark oak look and feel of a bank branch is a thing of the past.

Nearly all of our designs these days can be labeled “modern” – with natural earth tones either being the primary style, as seen in our work with Northeastern Credit Union, or where earth tones are a highlight of the overall design, as seen in our recent work with Champion Credit Union.

CURBSIDE

What Target Is Doing

Target is doubling down on the idea of curbside, where orders can be made online. Time-crunched shoppers can pull up to a designated spot and have orders brought out to them without leaving the car.

While many Targets already do this,

Translating This Into Retail Branching Terms

We have already spoken about the rise of Curbside at the branch, and this further solidifies the notion that there is very much a play for a Curbside feature at a branch.

When you factor in the overall customer experience, the need for speed and efficiency, and you sprinkle in a little bit of COVID-19’s legacy in retail, converting some existing parking spaces into a Curbside function featuring ITM’s makes a lot of sense.

You can still deliver on the cash transaction needs, but introduce video chat with Universal Tellers inside the branch. They can even come out to the car and meet customers for a handful of needs. It is a tremendous way to continually evolve the branch.

If you want to learn more about how design can help elevate your overall branch, contact us today.

Micro Branch Strategy – The Full Series

- Branch Transformation

- Retail

Categories:

Previously, we released our take on Curbside Banking, a supplement to the previously released “Branch Design After COVID-19” Guide Book. Both have been incredibly well-received and we’re grateful for all who have read it and reached out to us to learn more.

Within the Curbside Banking supplement, we introduced a new Micro Branch concept. While we have done previous posts on Micro Branches, we thought we would return to this topic. This time we’ll focus on 3 underlying strategies that are often overlooked when considering going small.

First, in Part 1, we are going to begin with the “Network Effect.” What is the Network Effect? Funny you should ask, that’s what we’re here to talk about.

The traditional economist states that the more people use something, the more valuable that it becomes.

In the retail banking world, Bancography states the following:

“The network effect is the phenomenon by which large branch networks capture a disproportionate share of market deposits. For example, a four-branch network captures more than twice the deposit volume of a two-branch network; an eight-branch network captures more than twice the deposit volume of a four-branch network. Viewed another way, average deposit size per branch increases as a function of the number of branches, as each incremental branch a financial institution adds provides a lift to – and derives benefit from – all its preexisting branches in the market.” – Bancography, April 2017

In other retail terms, it answers the question of why there is always Starbucks across the street from every Starbucks. When you see one on every corner, you start to want Starbucks. Saturating a market with brick and mortar has an exponential growth metric attributed to that strategy.

So, let’s now bring this back to your Retail Branch growth strategy and how the Micro Branch plays a role.

When you operate a network of branches in a given market, there is an assumed volume of Loans and Deposits that are up for grabs. When we run our consulting engagements, we estimate a Market or Trade Area’s total forecastable Loans and Deposits volume. From here, we estimate what your “fair share” is and what is also available. This availability is where your branch expansion plans come in.

While building several full-scale, standalone branches is ideal, this is not always feasible. Do you lack the available capital for a series of additional free standing branches, but want to capitalize on the Network Effect? A Micro Branch may very well be the perfect answer.

A Micro Branch can often cost 1/3rd the price of a free standing branch, yet allows you to further penetrate and saturate a market. This addition of low-cost brick and mortar locations allows you to expand your brand, serve your customers/members, and grab available Loans and Deposits in that market. A compounding effect will take place with each additional location because of the Network Effect. This will aid the percent increase of those Loans and Deposits at the locations already in existence.

Now onto Part 2, where we’ll go beyond the single market notion of the “Network Effect” and discuss an expanded concept. We’ll debate whether or not it makes sense to enter a new market and how the Micro Branch plays a role in this decision. Since this new, expanded version of the Network Effect doesn’t really have a name, we’ll call it the “Out of Network Effect.”

Many times, when we’re engaged in a Multi-Site Branch Growth Plan consulting engagement, we discuss geographic expansion strategies. A scenario always arises that proves to be a bit of a conundrum.

When we assess large, county-wide, or even state-wide geographies in an effort to find the best Trade Areas for branch expansion, there are some markets where the data implies a branch makes a lot of sense. Then, there are other Trade Areas that do not justify a fully staffed standalone branch.

This is where the Micro Branch comes into play – especially when considering the Out of Network Effect.

To further explain, I’ll use a recent example from a current client where this played out. I’ll be as specific as I can while maintaining our client’s privacy.

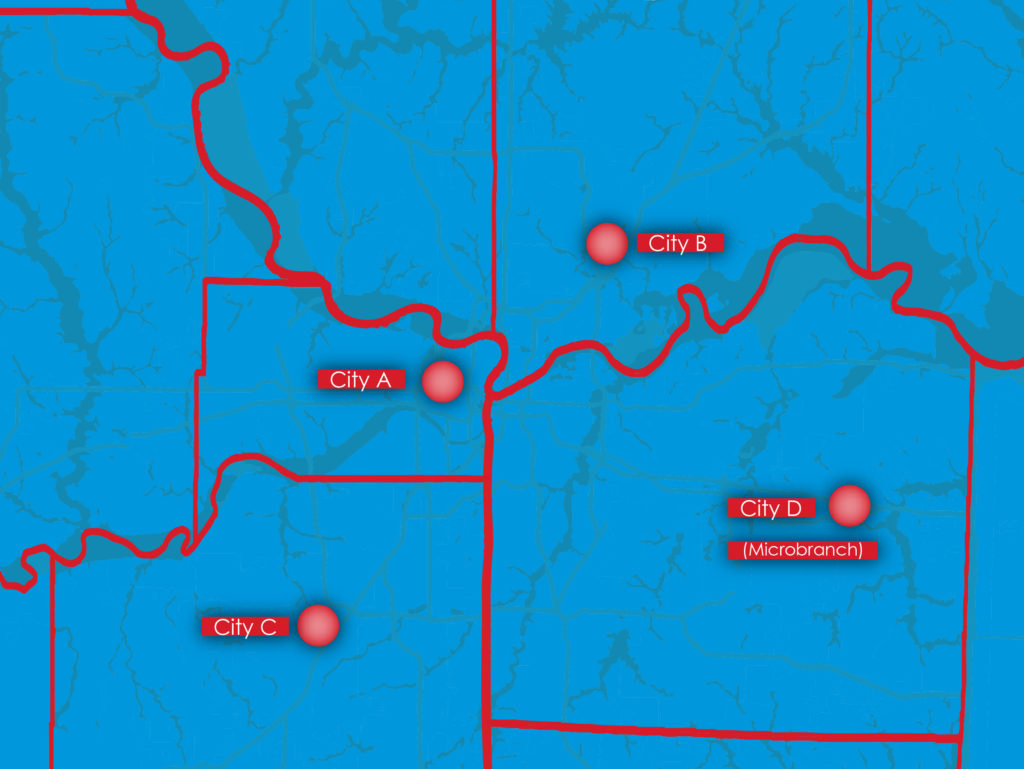

We recently executed a Multi-Site Branch Growth Plan where we looked at 4 cities across 4 counties. Each city represented the county seat, with one of these cities being a large metropolitan area. The remaining 3 cities were rural outposts with residents either working locally or commuting into the “big city.”

City A represents the large metropolitan area, where our study indicated the optimal number for the Network Effect at 6 branches. City B is their Headquarters branch, with a total Network Effect need at 3 branches. City C is a net new market, with a total Network Effect also at 3.

This is where the conundrum arose with City D. The data show that many employees and customers of this company live in City D. Yet, based on our Loans and Deposits forecasting, the data does not support a full standalone branch in City D.

But – the data does support a Micro Branch.

Executing a Micro Branch in City D is a win on several levels:

- It takes a cost-effective approach to branching, thanks to the smaller footprint and lower overhead costs of a Micro Branch

- It serves the needs of local customers, regardless of reduced loans and deposits compared to larger, neighboring towns

- It will aid in the Network Effect, but in this case, benefiting from the Out of Network Effect

Here’s why a Micro Branch makes sense in this smaller town. If you think about it, the Network Effect states that there will be a total lift in sales (Loans & Deposits) in a given market by adding locations and aiding total saturation. This economic philosophy typically works for a confined market.

When you expand this to a rural, multi-county setting in addition to a dense metro market, the theory still holds. People who live in a tightly packed metro market need not venture more than a couple miles beyond their home’s radius. When you live in the country, however, you’re often driving across county lines. Wether it’s for a job, to see family, to get groceries, or visit specialty shops, it’s always a journey.

That’s why we did not recommend a standalone branch in City D, despite the client stating they wanted one. The data did not support it. Since we ran a proforma on a Micro Branch, however, the client got the branch they desired. Not only that, but all other branches in the quad-county analysis benefited from this single Micro Branch. Thus, the Out of Network Effect took hold.

Now here in Part 3, we’re going to revisit the concept of Hub & Spoke. This time, we’ll discuss how the Micro Branch can play an important role in executing this concept.

For visual purposes, we’re going to use a generic Market Area for Anytown, USA. These strategies can not only work for any given metro market, but can also be applied across a more rural, multi-county geography.

First, let’s revisit the concept of Hub & Spoke.

On the surface, the Hub & Spoke retail branch model implies you have your bigger branch as a central anchor (hub) to smaller, scattered satellite branches (spoke) across a given geography. Implying that Hub & Spoke is only about branch size, however, is missing the point.

When thought of strategically, the right Hub & Spoke model is about efficiencies while considering:

- Serving Your Clients – Having locations where your clients live and work provides the convenience they require of you, even if some are digital first. Beyond location convenience, you can further serve your clients by understanding demographies of given neighborhoods. More specifically, know their propensities for products and services so that you can offer what your clients need and make adjustments across different spokes.

- Network Effect – To reiterate from our previous posts, saturated markets and/or trade areas may allow the addition of more spokes. This would complete your Network Effect strategy and, in effect, elevate all other locations along the way.

- Budget Considerations – Factor in these elements and the cost considerations of a Micro Branch compared to a freestanding branch. You’ll find that you get a lot of lift out of a Micro Branch. It is a much more effective notion especially if you’re unable to afford a traditional branch at a specific site.

All of this is where having a Micro Branch as your wild card really comes into play.

When looking at the Hub & Spoke model across your branch network, your Hub is the flagship; the crowning achievement. It is the branch with the best design. It offers the most services, has best employees, and is either located in the optimal neighborhood or in the neighborhood with the best bragging rights (many traditional retailers put their flagship stores in Times Square (New York City), Union Square (San Francisco) or Magnificent Mile (Chicago)).

Your spokes are the soldier locations spread across the field. When the data doesn’t support a full branch in the outposts of your empire, the Micro Branch is ready to swoop in and fill the void.

The last point we’ll make here to close out this article and the series is this: the Hub & Spoke model actually has two sides.

- Side #1 is your entire branch network, anchored by your Hub Flagship branch and bespoked across your geography. If you are a Community Bank or Credit Union, this is your strategy. You operate a fleet of branches typically in one larger geographic market.

- Side #2 is is more cluster based, allowing for multiple instances of a Hub & Spoke model. You will have multiple Hubs and their aligned spokes across different geographies. If you are a larger FI, one that spans across different metropolitan areas or state lines, deploying this type of Hub & Spoke model may make sense. For example, you may have a Hub and several spokes in Dallas, and another wave of Hub/Spoke branches in Houston.

To learn more about how Micro Branches can help you complete a well-rounded Hub & Spoke strategy, Contact Us today to learn about our Data Driven Consulting division and how the right branch strategy can help you double in size.

Micro Branch Strategy – Part 3

- Branch Transformation

Categories:

In our final article on Micro Branch Strategy, we’re going to revisit the concept of Hub & Spoke. This time, we’ll discuss how the Micro Branch can play an important role in executing this concept.

For visual purposes, we’re going to use a generic Market Area for Anytown, USA. These strategies can not only work for any given metro market, but can also be applied across a more rural, multi-county geography.

First, let’s revisit the concept of Hub & Spoke.

On the surface, the Hub & Spoke retail branch model implies you have your bigger branch as a central anchor (hub) to smaller, scattered satellite branches (spoke) across a given geography. Implying that Hub & Spoke is only about branch size, however, is missing the point.

When thought of strategically, the right Hub & Spoke model is about efficiencies while considering:

- Serving Your Clients – Having locations where your clients live and work provides the convenience they require of you, even if some are digital first. Beyond location convenience, you can further serve your clients by understanding demographies of given neighborhoods. More specifically, know their propensities for products and services so that you can offer what your clients need and make adjustments across different spokes.

- Network Effect – To reiterate from our previous posts, saturated markets and/or trade areas may allow the addition of more spokes. This would complete your Network Effect strategy and, in effect, elevate all other locations along the way.

- Budget Considerations – Factor in these elements and the cost considerations of a Micro Branch compared to a freestanding branch. You’ll find that you get a lot of lift out of a Micro Branch. It is a much more effective notion especially if you’re unable to afford a traditional branch at a specific site.

All of this is where having a Micro Branch as your wild card really comes into play.

When looking at the Hub & Spoke model across your branch network, your Hub is the flagship; the crowning achievement. It is the branch with the best design. It offers the most services, has best employees, and is either located in the optimal neighborhood or in the neighborhood with the best bragging rights (many traditional retailers put their flagship stores in Times Square (New York City), Union Square (San Francisco) or Magnificent Mile (Chicago)).

Your spokes are the soldier locations spread across the field. When the data doesn’t support a full branch in the outposts of your empire, the Micro Branch is ready to swoop in and fill the void.

The last point we’ll make here to close out this article and the series is this: the Hub & Spoke model actually has two sides.

- Side #1 is your entire branch network, anchored by your Hub Flagship branch and bespoked across your geography. If you are a Community Bank or Credit Union, this is your strategy. You operate a fleet of branches typically in one larger geographic market.

- Side #2 is is more cluster based, allowing for multiple instances of a Hub & Spoke model. You will have multiple Hubs and their aligned spokes across different geographies. If you are a larger FI, one that spans across different metropolitan areas or state lines, deploying this type of Hub & Spoke model may make sense. For example, you may have a Hub and several spokes in Dallas, and another wave of Hub/Spoke branches in Houston.

To learn more about how Micro Branches can help you complete a well-rounded Hub & Spoke strategy, Contact Us today to learn about our Data Driven Consulting division and how the right branch strategy can help you double in size.